30 kilometres that can bring the world economy to its knees

The Strait of Hormuz is a bottleneck between Iran and Oman – barely 30 kilometres wide, only about 8 kilometres navigable. Through this narrow corridor flow 20 to 30 per cent of global oil and gas transport. Kuwait, Saudi Arabia, Iraq, Qatar, the United Arab Emirates – the world's largest energy exporters depend on this passage. When Iran enforced the blockade, that was not a symbolic gesture. It was an economic attack on global energy supply, and it works. For European businesses that may sound abstract: only about 13 per cent of European LNG and oil imports come directly from Gulf states. But the oil market is global. When a third of global supply is disrupted, prices rise everywhere – regardless of where you source yourself. That is not theory. That is what is happening now.

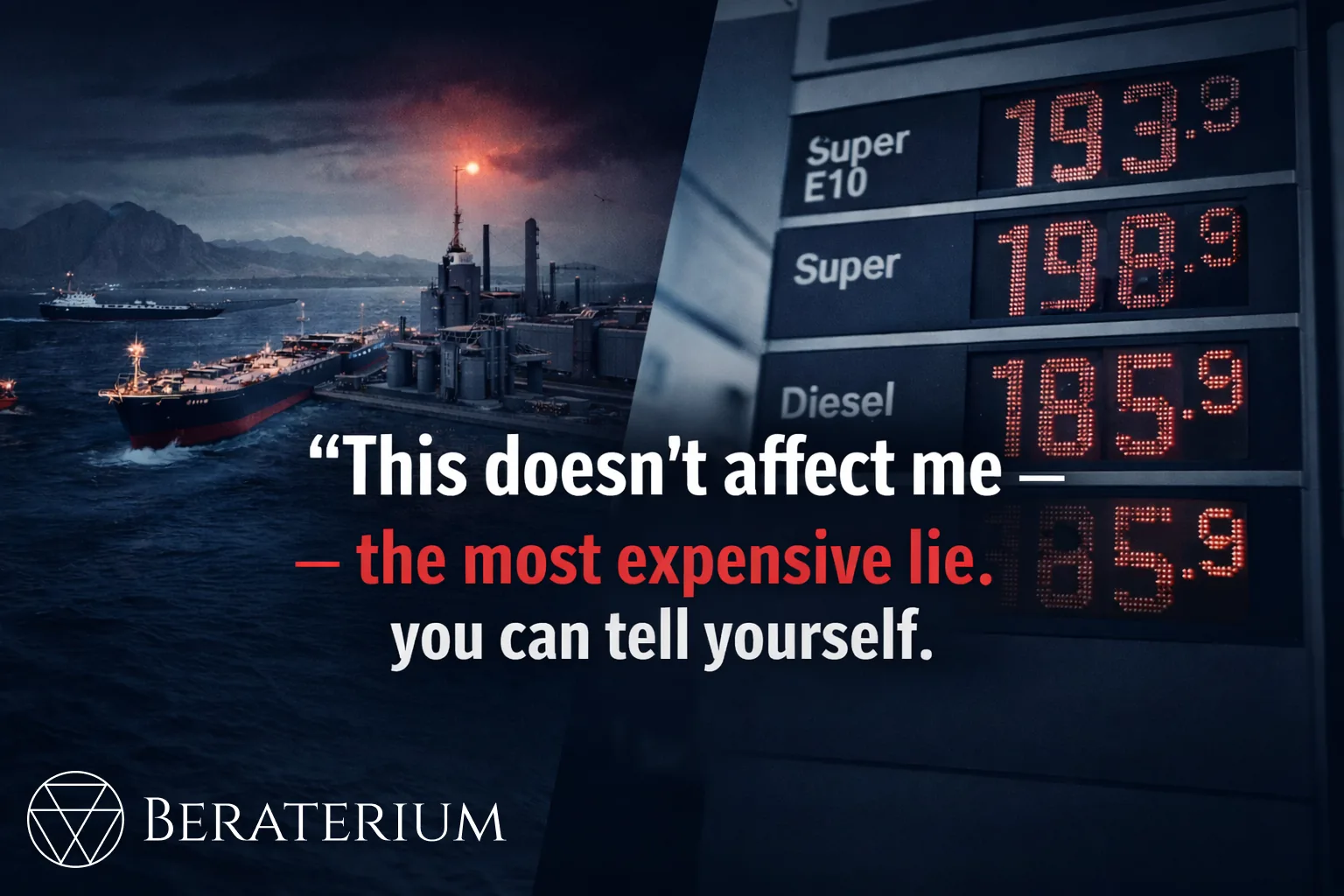

What does a 40 per cent price rise cost – in your business?

The figures are clear: the crude oil price rose within one month from around 70 USD to over 120 USD per barrel – an increase of almost 70 per cent. And that is not the end. Iran has publicly stated the target is an oil price of 200 USD per barrel. That sounds like propaganda, but the trend points exactly that way. In Germany the petrol price rose in a few weeks from about 1.70 euros to over 2 euros per litre – more than 30 cents extra. For private consumers that is annoying; for a farmer who puts 100 litres of diesel in the tractor daily, that is 50 to 100 euros extra per day if it is even enough. For a transport company, a haulier, a craft business with field service – everywhere these costs eat margins. And they are passed on: to suppliers, customers, the end consumer. This spiral is already in motion.

Why China is your problem – even if you buy nothing there

China officially imports no oil from Iran. Unofficially it looks different: around 14 to 15 per cent of Chinese oil imports come from Iran, another 4 to 5 per cent from Venezuela – both countries whose exports are now under massive pressure. China refined this cheap, not high-quality oil and sold it on as petroleum products – a profitable business that is now breaking down. Petrol prices in yuan have also risen sharply in China. But the real problem for German businesses is different: when production costs in China rise, prices rise for everything that comes from China. And that is more than many believe. Whoever thinks they are independent of China has usually not looked deep enough into their own supply chain. Another risk few have on the radar: when bottlenecks arise in China, Beijing prioritises the domestic market. Exports are throttled or stopped – perhaps only for a week, but on sea routes that quickly becomes three to four weeks' delay.

Fertiliser: the silent crisis that ends on the supermarket shelf

It is tempting to lean back and say: my suppliers are local, my customers are here, Iran is far away. That stance is negligent. Take a welding business: the steel comes from the local supplier – so far, so good. But where does the steel really come from? Increasingly from China. Welding equipment, laser technology, computers in the business, staff mobiles – all global supply chains. Even if your own company has no direct international suppliers: your suppliers' suppliers are almost always globally networked. And that is exactly where it breaks first – invisibly, until it is too late. Whoever today says "we've done it this way for 20 years, it'll be fine" has not understood how fragile the system has become. Since January 2026 alone the geopolitical situation has changed so dramatically that any static risk view is outdated.

"It doesn't affect me" – the most dangerous misjudgement

People talk about oil prices. Hardly about fertiliser. Yet here lies the lever most underestimate: 40 to 45 per cent of global urea exports – the base for phosphate fertilisers – go via the Strait of Hormuz. Iran itself produces around 10 to 15 per cent of global urea. Prices have risen from about 550 USD to 680 USD per tonne – a jump that runs through the entire food chain. The farmer pays more for fertiliser. More for diesel. More to transport the harvest. These costs end up in the supermarket, in our trolley. It does not happen immediately – price rises need weeks to months to seep through – but the mechanism is unavoidable. And it affects not only Germany, but all of Europe.

Dubai crashing – and what that means for your risk view

An example showing how fast perceived safety can change: the property market in Dubai is experiencing a massive slump. Not because missiles are hitting there – but because they could. People who emigrated to the Emirates are now trying to offload property and return to Germany. From one day to the next. The same applies to businesses that source freelancers from India or Pakistan: when an energy crisis breaks out there, people may no longer work on your website but look after their family's survival. These are not hypothetical scenarios – they are happening now. And they show that risk assessment must not stop at the company door. Whoever thinks globally – in procurement, people, investment – must also view risks globally.

People at the centre: why risk management starts with staff

Amid all the figures and supply chain analysis, one factor often fades: the person. When petrol prices rise, it hits the commuter with a long journey whose pay is already tight. Perhaps they eventually say: I'll find something nearer. If you employ skilled staff from Iran, the Gulf states or other affected regions, you must understand: these people have their minds on family. They may want to bring relatives to safety, support them, they cannot simply carry on as if nothing were happening. The answer is not pressure, but humanity. Better a few days off so someone can look after emotions and family than an unfocused employee who is already elsewhere inside – or who resigns. Without staff no business runs. And whoever believes the human factor plays no role in risk management has not understood risk management.

Plan B is not enough – you need Plan C

The quintessence from this crisis is uncomfortable: Plan B is no longer enough. Whoever operates in a world where geopolitical conflicts within weeks translate into rising supermarket prices needs Plan C too. Just-in-time logistics works in 98 per cent of cases – until a bridge collapses, winter hits or a strait is blocked. German businesses have optimised over decades: stock reduced, supply chains trimmed for efficiency, buffers eliminated. That made economic sense – until it did not. It is not about building warehouses everywhere again. It is about analysing intelligently: what is really essential? Where are the real dependencies? What does it cost me per week if something fails? And then smart heads must sit together and develop measures that fit current reality – not reality from five years ago.

What to do now: 5 concrete steps

1. Take a 360-degree view: Do not only look at your own suppliers, but their suppliers – and theirs. Where do raw materials really come from?

2. Calculate costs: What does it cost if energy is 40 per cent more expensive? What if a supplier cannot deliver for two weeks? Quantify in euros, not gut feeling.

3. Keep staff in view: Who commutes far? Who has family in crisis regions? Who might leave when load rises?

4. Create buffers: Do not blindly build stock, but check critical materials and specialist tools on reserve. One missing specialist part can shut down whole production.

5. Update regularly: Ticking ISO checklists once is no longer enough. Risk assessment must be an ongoing process – at least quarterly, more often in acute crises.

Conclusion

The Iran crisis shows sharply: in a globalised world there are no isolated conflicts. 30 kilometres of strait are enough to double oil prices, hit supermarket prices and unsettle skilled staff. Whoever as an entrepreneur today says "doesn't affect me" has not avoided the risk – only not seen it. Risk management does not start with the ISO norm. It starts with looking beyond your own plate – and with the person at the centre.